What Happens With a Reverse Mortgage When My Parents Die

More seniors are turning to a Home Equity Conversion Mortgage (HECM), also known as a reverse mortgage, to help them through their retirement years. Adult children may be concerned about what may happen to their parents’ home, which has a reverse mortgage loan, once either one or both of their parents die and how the loan should be resolved. Here are some frequently asked questions to help you.

Can my parents leave me their home?

Yes. Borrowers can still leave the family home to their heirs. The heirs have the option of keeping the home and paying off the loan or selling the home to pay off the loan when their parents die.

What happens with the reverse mortgage loan after my parents pass?

If you are an heir, you will receive a letter from the loan servicer explaining the guidelines and asking you what you intend to do with the property.

How quickly is the reverse mortgage loan due when my parents die?

A reverse mortgage becomes repayable once the last borrower or owner passes away. This doesn’t give you, the heir, much time to refinance or sell the home, so it’s important to stay in close contact with the loan servicer as times vary. Answer questions to the best of your ability as not to slow the process down so that the loan goes into default.

What happens if I want to keep the home?

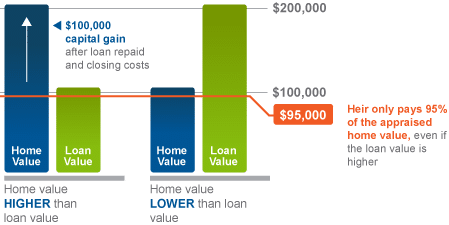

If you want to keep the home, you will need to pay off the loan. You can choose to refinance the home or you can sell the home. You can manage the sale and keep any capital gain after the loan and closing costs have been paid.

What happens if the property is worth less than the loan, will it affect my assets?

One plus to a reverse mortgage is that you won’t owe more than 95% of the home’s appraised value, even if the loan balance is more than that. HECM’s are “non-recourse” loans. Therefore, if you sell the home to repay the loan, you will never owe more than the loan balance or the value of the property, whichever is less; and no assets other than the home will be used to repay the debt.

Basically this means that if the value of the home is less than the mortgage balance, you are not responsible for the difference. This is particularly important during recessions when property values have fallen. Furthermore, you will never be required to use your personal assets to pay off the loan.

Example: Say the home declined in value during the housing slump and the loan now exceeds the home’s appraised value – the home is appraised for $100,000, but the loan balance is $200,000.

To KEEP the home, you will need to pay $95,000 (95% of the $100,000 current market value).

You do NOT have to pay the full balance; the FHA Mortgage Insurance covers the remaining loan amount.

If you decide to sell the house, the home must be listed at a minimum of the appraised value. Because all sale proceeds go to pay off part of the loan and real estate fees, the estate receives no equity. The FHA Mortgage Insurance picks up the difference on the loan.

What if I don’t want the home?

If you don’t want the home after the death of your parents, you have a couple of options. Within 30 days of notification, the lender will send an FHA appraiser to determine the home’s current market value. You have 60 days to sell the home or forfeit without penalty. You can request two 90-day extensions with the lender and another two 90-day extensions with FHA.

To receive the full 12 months (1 year) extension you must show evidence that you are actively trying to sell the house, such as providing a listing document or sales contract.

If there is no potential equity, you may decide to simply hand the keys to the lender and avoid the hassle of trying to sell the home. Known as “Deed in lieu of foreclosure,” you will need to sign the deed over to the lender, forfeiting any possible remaining equity. You are however; protected by the FHA Mortgage Insurance to not owe any remaining debt if the home cannot be sold for the amount of the loan balance in the foreclosure sale.